In June 2025, Cognition charged $500 a month for Devin, its AI software engineer. By early 2026 the entry price was $20. A 96% cut in under a year, and two forces drove it. From below, open-weight models out of Chinese labs, DeepSeek, Qwen, Kimi, and GLM, now do frontier-grade work for a rounding error: DeepSeek's V4 Flash serves a million output tokens for 28 cents, against $25 to $30 for the flagships at OpenAI and Anthropic. From the side, well-funded players treat frontier access as a loss leader to buy market share, which is why Devin's own cut reads less like a discount and more like a land grab.

Anthropic, over the same stretch, is raising near a trillion-dollar valuation. The labs that sell the raw brain are becoming some of the largest companies on earth. The agents built on top of them are racing toward free.

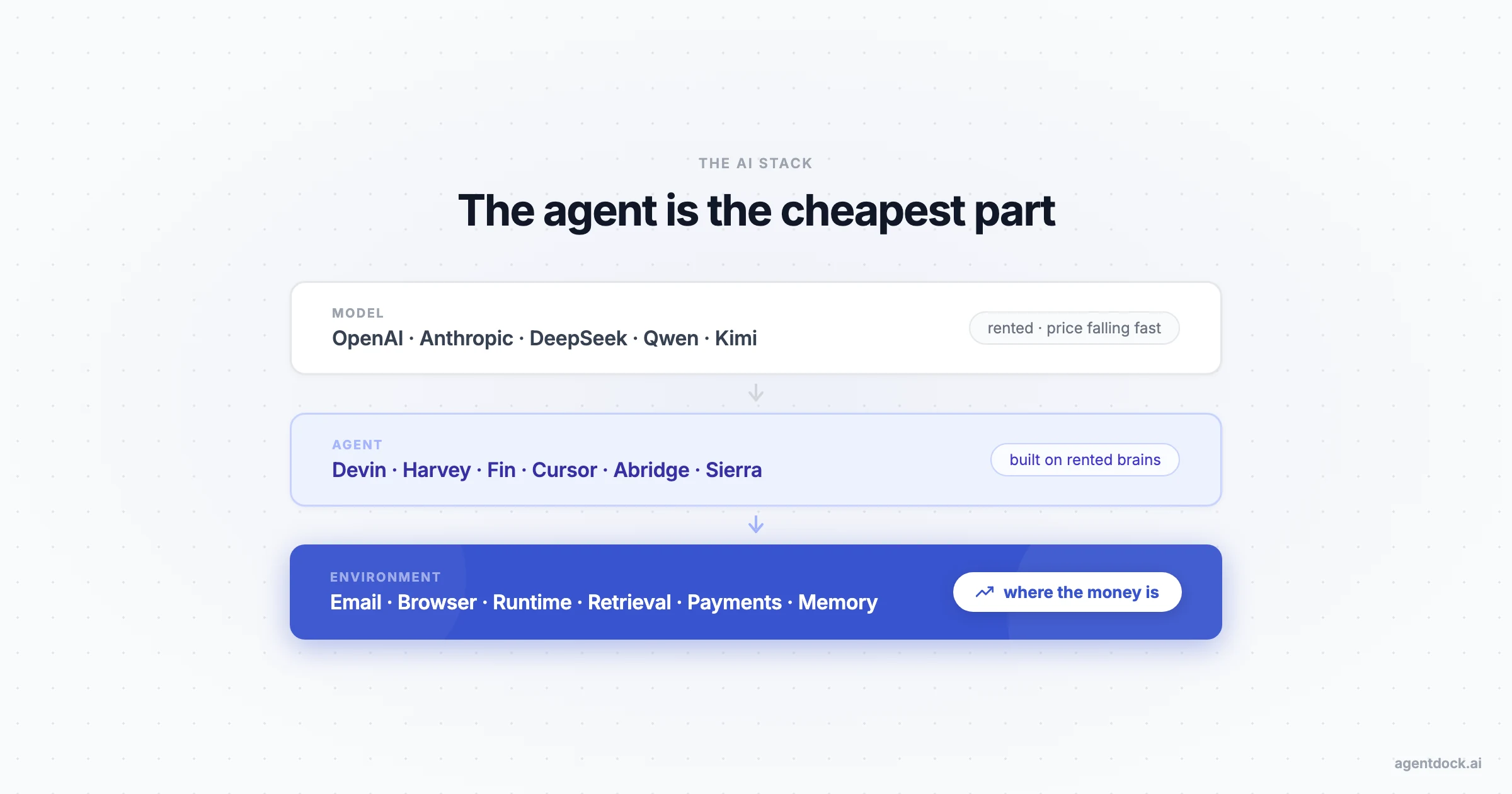

That gap is the whole story for anyone trying to make money here. The agent is the cheapest part. The money is in what surrounds it: where the agent runs, the surfaces it works through, and the rails it pays and gets paid on.

The popular version of this is Sequoia's "services are the new software." Sell the finished work, bill against the labor budget instead of the software budget. True, and already crowded. The less obvious money sits one layer over, in the environment every one of those services has to rent.

For the record: 15+ years in software engineering leadership. I led Udemy's growth from near-zero to $100M+ in revenue through growth engineering, and I now build AI-employee products. These are the day-to-day observations I make.

The brain is a rental

There are two places you can rent a frontier brain, and a handful catching up fast. Anthropic reported a $47 billion run rate in May 2026 on a gross basis. OpenAI sits near $33 billion. The two argue about accounting, and on OpenAI's preferred net math Anthropic is closer to $22 billion. Tens of billions either way, both climbing toward a trillion-dollar valuation.

For anyone building on top, that is a gift. You can rent a frontier model for the cost of an API call, or self-host an open-weight one for the price of electricity, around $0.20 to $0.50 per million tokens. The labs and the agent startups are racing each other down, some pricing below cost to buy share. It turns into your problem only if your edge was being smart. The smartness is rented, and the rent keeps falling. Your competitor rents the same brain on Monday.

So the question that lasts is not how clever your agent is. It is what your agent touches that the model cannot carry with it. A model has no inbox, no browser, no memory of yesterday's conversation, no payment rail, no customers. Those you can own.

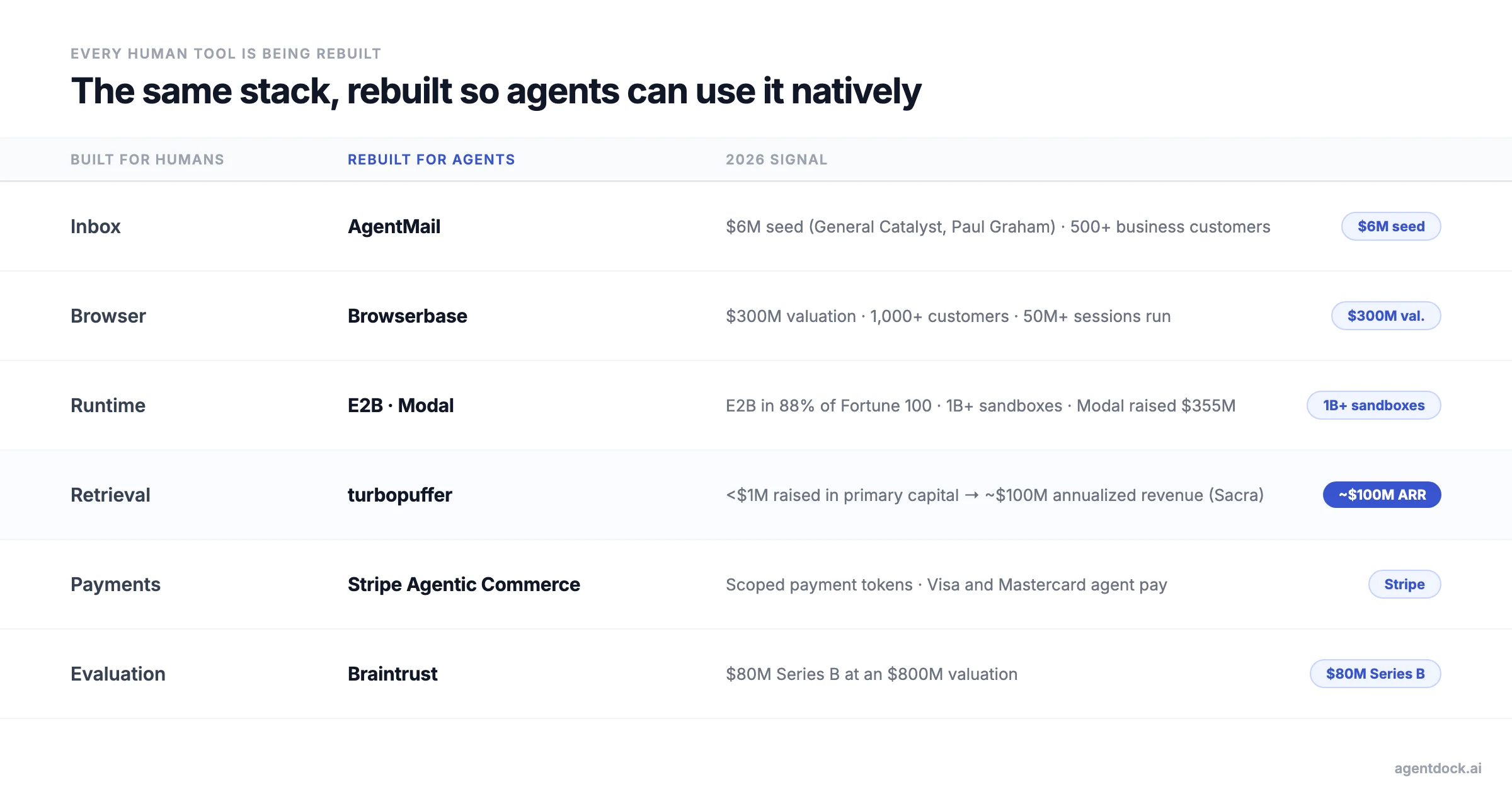

Every human tool is being rebuilt for agents

The fastest money is forming in tools that already existed for people, rebuilt so an agent can use them directly.

Email is the clean case. AgentMail raised $6 million in March 2026, led by General Catalyst, with Paul Graham and HubSpot's Dharmesh Shah in the round. It gives an agent its own inbox over an API, no human screen attached, and already serves more than 500 business customers. Gmail was built for a person checking mail. AgentMail is built for a process that never sleeps. Browserbase did the same for the browser, running over 50 million sessions for more than 1,000 customers like Perplexity and Vercel. Stripe did it for checkout, so an agent pays with a scoped token instead of a human typing a card.

The same rebuild is running across the stack:

| Human tool | Rebuilt for agents | 2026 signal |

|---|---|---|

| Inbox | AgentMail | $6M seed (General Catalyst, Paul Graham, Dharmesh Shah); 500+ business customers |

| Browser | Browserbase | $300M valuation, 1,000+ customers, 50M+ sessions |

| Runtime | E2B, Modal | E2B in 88% of the Fortune 100, 1B+ sandboxes run; Modal raised $355M |

| Retrieval | Turbopuffer | Under $1M raised, ~$100M annualized revenue (Sacra estimate); powers Cursor and Notion |

| Payments | Stripe Agentic Commerce | Scoped payment tokens; Visa and Mastercard agent pay |

| Evaluation | Braintrust | $80M Series B at an $800M valuation |

| The model | Anthropic, OpenAI | ~$47B run rate, nearing $1T. The part you rent, with open weights pushing it toward cost. |

One number reframes the market. Turbopuffer, the search layer behind Cursor and Notion, has raised under $1 million in primary capital and reached roughly $100 million in annualized revenue, by Sacra's estimate. Cursor, the agent on top, has raised billions to grow. Anthropic, the brain underneath, raised tens of billions. The best capital efficiency in the entire stack sits in the unglamorous middle, the environment, not the agent.

This is the old bundling question in new clothes. The infrastructure is unbundling, with email, browser, retrieval, and payments each becoming their own company. The outcome bundles back up, which is why Sierra sells a whole "Agent OS" rather than a piece. One caution: the clouds are re-bundling that infrastructure fast, with AWS, Google, Vercel, and Cloudflare all shipping agent sandboxes inside a single quarter. Owning a surface is good. Owning one a hyperscaler can clone in ninety days is not.

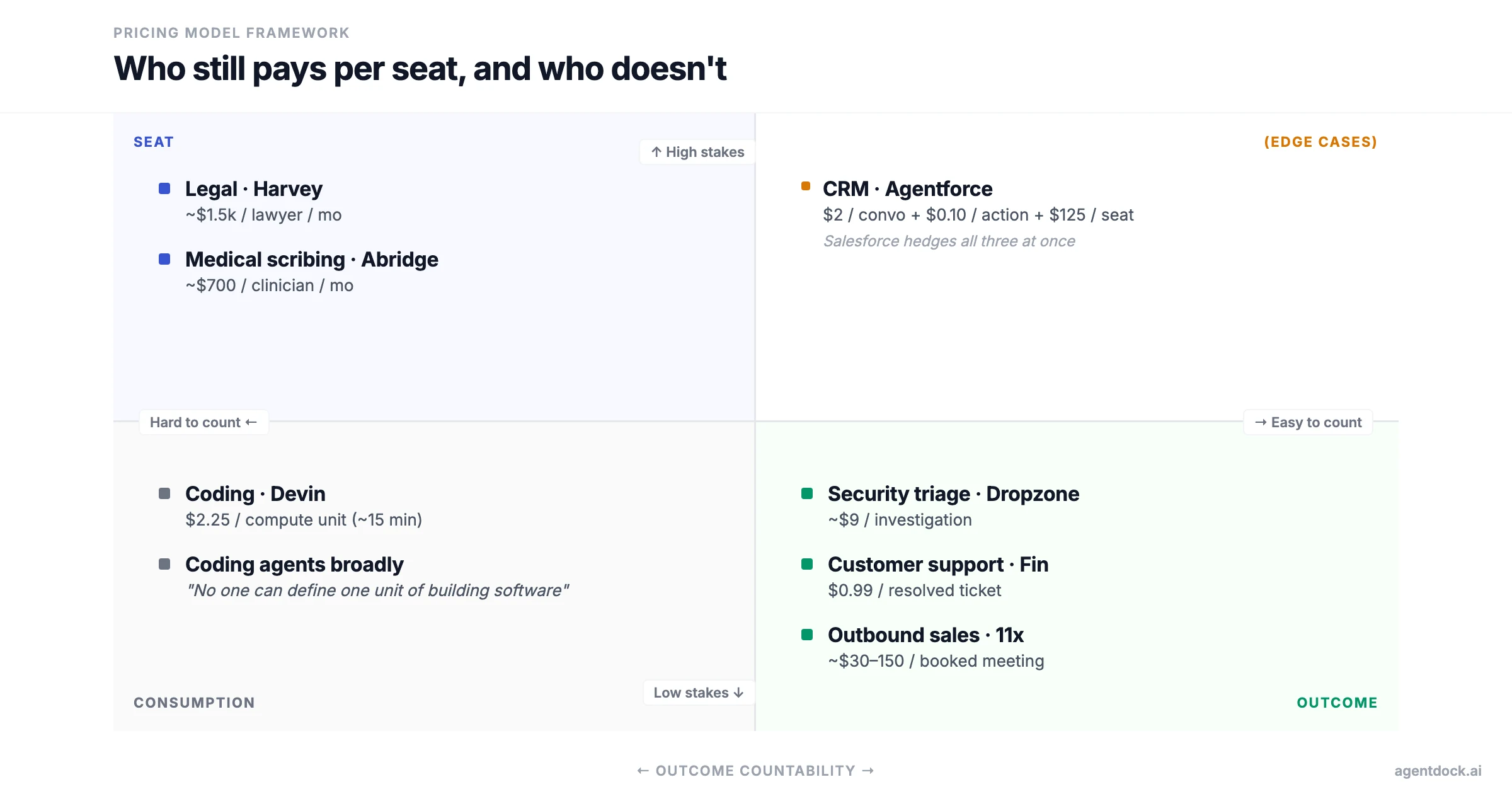

The seat isn't dead. It's outnumbered.

Here is the part most people get backwards. Half the market says the per-seat subscription is finished, replaced by pay-per-outcome. That is half right. Pricing is splitting three ways, and the split lines up with one thing: how cleanly you can count the result.

Where the result is a clean, countable, low-stakes event, outcome pricing wins. Intercom's Fin charges $0.99 per resolved ticket. Sierra charges a pre-negotiated rate per resolution and nothing when it hands the case to a human. In security, Dropzone runs about $9 per investigation and Prophet about $10. In outbound sales, 11x rents a digital worker for around $5,000 a month, which pencils out near $30 to $150 per booked meeting. The unit of sale is the finished job.

I led the engineering behind Coinbase Custody's integrations and client interfaces while it grew assets under management 20x, working hand-in-hand with support there and at Udemy. So here is what those per-resolution price tags hide. A resolution is not a clean number. Whether a ticket counts as resolved, and who pays when the customer writes back the next day, is the real fight. Charging $0.99 a resolution is a bet that you can define a word your customer will dispute.

Where the work is open-ended, consumption pricing wins. Cognition meters Devin in compute units at $2.25 each, about fifteen minutes of work apiece. You pay for effort, because no one can define one unit of "building software."

Where judgment and liability run high, the seat holds. Harvey, the legal AI, still charges a reported $1,000 to $2,000 per lawyer per month. Abridge, the medical scribe, runs around $600 to $800 per clinician. No firm will pay per correct legal opinion, and no hospital will pay per diagnosis. The seat survives because the outcome is too fuzzy and the downside too severe to meter. Even Salesforce hedges, shipping Agentforce with a $2 conversation, a $0.10 action, and a $125 seat at the same time.

| Job | What you pay for | Price | Pattern |

|---|---|---|---|

| Customer support | the resolution | Intercom Fin $0.99; Sierra free on handoff | Outcome |

| Security triage | the investigation | Dropzone ~$9, Prophet ~$10 | Outcome |

| Outbound sales | the meeting | 11x ~$5,000/mo, ~$30-150/meeting | Outcome |

| Coding | the compute unit | Devin $2.25 per ACU (~15 min) | Consumption |

| CRM (Agentforce) | all three at once | $2/conversation, $0.10/action, $125/seat | Hybrid |

| Legal | the seat (reported) | Harvey ~$1,000-2,000 per lawyer/mo | Seat holds |

| Medical scribing | the seat (reported) | Abridge ~$600-800 per clinician/mo | Seat holds |

The rule is short. Countable and cheap to get wrong goes to outcomes. Open-ended goes to consumption. High-judgment goes to seats. Anyone who tells you the seat is dead has never priced a job where being wrong gets someone sued.

Your customer's agent is your customer

Here it gets uncomfortable. Once agents do the buying, your customer is not a person. It is an agent, working for a shopper or for a company, and it shops nothing like a human.

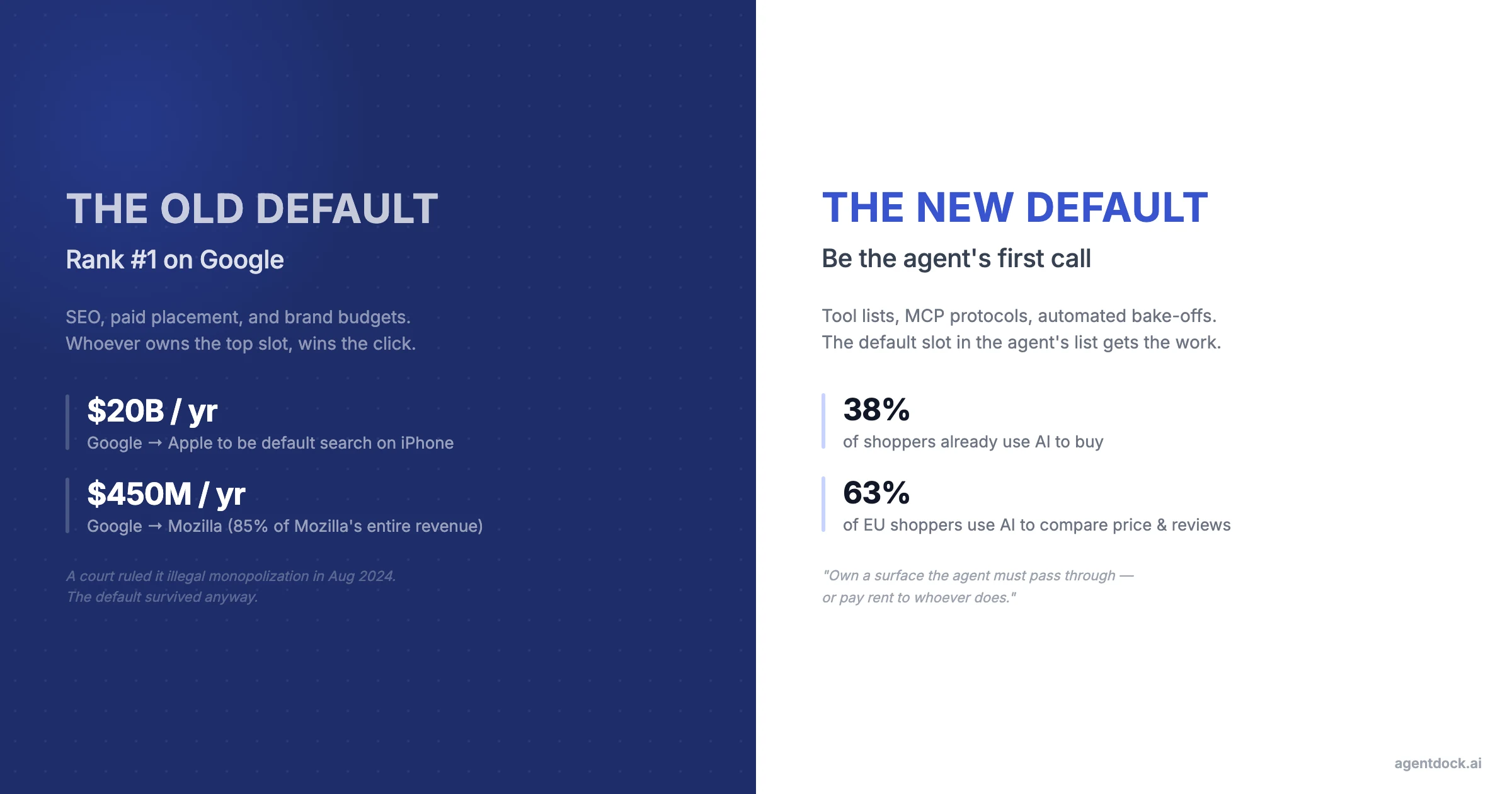

A person builds habits, remembers a brand, and stays with a worse option out of inertia. An agent rechecks the market on every request, because checking costs a fraction of a cent. Already 38% of shoppers use AI to buy, and 63% of European shoppers use it to compare price and reviews. Stripe now lets a merchant choose which agents to sell through. The agent chooses right back. Today that choice runs through a tool list and a model's recommendation. Whoever sits at the top of that list, by default, gets the call.

This runs in B2B too, and further along. Sometimes the buyer is the agent itself: through protocols like MCP, an agent picks which tool to call at runtime, and the default in that list gets the work. turbopuffer grew by sitting inside products like Cursor, not by out-selling a database incumbent.

It also rewrites procurement. A person trials two or three vendors before deciding. An agent spins up trials with ten, runs the same eval against each, and buys the winner by Friday, because every signup and test is now an API call. Sales stops being a deck and a steak dinner. You win the automated bake-off, or you never make the shortlist. Whether the chooser is a shopper's agent or a company's procurement agent, the contest is the same: the default slot.

Read one way, this is the healthiest market we have had. No brand coasts on a billboard. The cheaper, better product wins, because the agent has no ego and infinite patience to compare. Distribution stops being a contest over who shouts loudest.

That growth-engineering work at Udemy was, underneath, a contest to earn the recommendation. The agent era moves the same contest to the agent's default list.

Read the other way, it is the same toll booth in a new spot. Whoever owns the agent owns the default, and defaults get sold. Google pays Apple about $20 billion a year to be the default search on the iPhone. It pays Mozilla around $450 million, close to 85% of Mozilla's entire revenue. Booking and Expedia spend 31% and 50% of their revenue on marketing, much of it bidding for Google placement. A court ruled those default deals illegal monopolization in August 2024. The September 2025 remedy still let Google keep paying for default and banned only exclusivity. That is how valuable the default is. It survived being called a crime.

Both readings are true, and the tension is the opportunity. Agents clear out the old pollution, the SEO sludge and brand noise that clogged human channels. A new scarcity forms one layer up, in the agent's default list. The money moves from ranking first on Google to being the tool an agent reaches for without asking. You earn that by owning a surface the agent must pass through, or you pay rent to whoever does.

Where the rent goes next

None of this is settled, and two forces could bend it. If inference keeps falling tenfold, per-resolution pricing breaks too, because you cannot charge $0.99 for work that costs a hundredth of a cent. Pricing has to move from cost to value, and value is harder to defend. The clouds, meanwhile, keep absorbing the infrastructure layer, so today's independent surface can become tomorrow's checkbox inside AWS.

The bet, then, is narrow. Do not build the brain. You will not outspend a duopoly raising at a trillion dollars. Do not resell raw intelligence, since it rents for less every quarter. Own a surface an agent has to use, in a job where being wrong still matters, and become its default before a hyperscaler ships a copy.

That is the part worth building.

I am building toward a world where agents are a native part of daily life. The bet is on surfaces, workflows, and blueprint agents that help businesses save and make money, not on the model's brain.